Note: this was originally written 12/22/2022…the rates referenced in this are from back then.

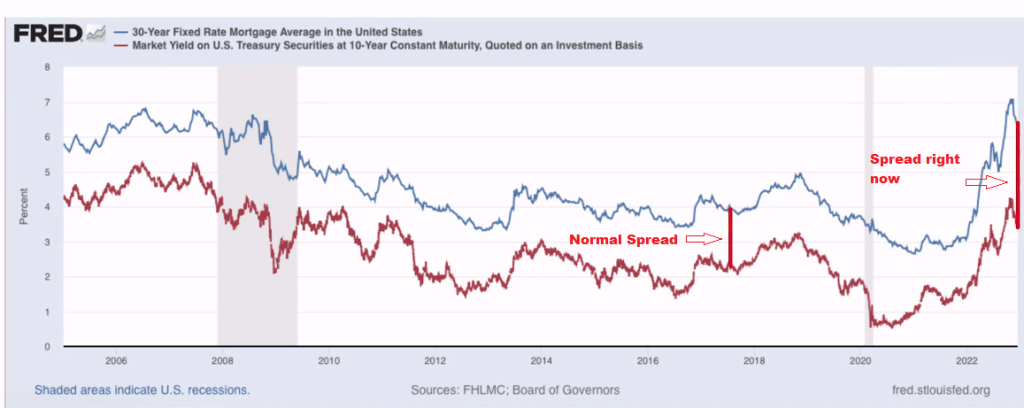

As covered in previous posts: mortgage rates are not cool this year. An underrated element of this though is that rates are actually worse than they should be. In the mortgage world, BondMarketBoys™ look to the 10 Year Treasury as a gauge for what mortgage rates should be. Going back 40 years, the historical spread between the 10 Year Treasury and 30 Year Fixed Mortgage averages between 1.75% and 2.00%.

In 2022 that spread has widened to near all-time highs, hitting 3.00%. Even with inflation moderating late in the year and mortgage rates slowly coming down, that high spread remains. So…what gives?

A wider spread indicates that the BondMarketBoys™ see signs of risk in the mortgage bond market…but not the kind of risk you’d usually associate with mortgages. The risk being priced in isn’t default risk, it’s prepayment risk. Meaning: if the market determines that there’s a high probability of a quick refinance they want to be compensated for that.

Originating bonds has a cost (time & money) and there’s a fair expectation that they’ll stay on the books long enough to recoup the cost to originate it. If there’s a belief that it won’t last long enough to recoup the cost (if it gets paid off…AKA “refinanced”…too soon) then the market will demand more fee upfront, which drives up rates, and widens the spread between that and the 10 Year.

In other words (and to oversimplify a complicated economic issue):

- Inflation is high which is bad for bonds

- To combat it The Fed is jacking up short term interest rates, and talking tougher than Biff Tannen (which creates long term volatility)

- Volatility creates uncertainty for interest rate sensitive markets that are freely prepayable – like mortgages

Once some semblance of predictability returns, it’s fair to assume that the spread between the 10 Year and the 30 Year mortgage should tighten to historical norms.

For perspective, using the historical spread, based on current 10 Year Treasury yields the 30 year mortgage rate should be 5.25% to 5.50% (around where the Mortgage Bankers Association projects the average 30 year mortgage rate to land next year).

Additional notes from 10/13/23: there are three things to note with the MBA’s prediction from 12/22/2022…

1). They were wrong (rates did not drop this year), but that was due to….

2). The 10 year treasury increasing by over 1% since then (not expected)

3). The spread between the 30 year fixed & 10 year treasury remaining above 3% (also not expected)

Leave a comment